Winning in Today’s Complex World

Key Societal Phenomena Have Evolved and Converged

To Transform the Culture of Out-of-Home Entertainment

By Randy White, CEO/White Hutchison Leisure & Learning Group

Three pivotal events and trends from 2006-2007 have evolved and converged to transform the culture of out-of-home entertainment into something a whole lot different than what is was back then, disrupting traditional formulas for location-based entertainment centers and resulting in the need for completely new business models.

2006 might be considered the beginning of the cultural foodie revolution. That was the year when social media began to take off (although we didn’t yet have “foodporn”). That was when food television shows like Top Chef and No Reservations made the idea of being a chef cool. That was the year that saw the rise of food bloggers like Eater and Serious Eats, giving restaurants a 24/7 news cycle, making chefs into celebrities and raising the public’s interest in new culinary experiences.

Two years later in 2008, the food revolution continued to evolve when then-unknown chef Roy Choi launched the first “foodie” food truck in Los Angeles featuring Korean-Mexican fusion tacos called Kogi BBQ and started using Twitter to let people know where the Kogi truck was going to be serving: posting multiple times per day, even per hour about their location and specials.

Then in 2010, we saw the first foodporn photos posted on Instagram. Since then, the public’s pursuit of adventure and discovery with food and drink has mushroomed to where we are today with the majority of Americans (53 percent) now considering themselves foodies. The expectations and culture of dining and drinking out has changed forever.

The second pivotal event took place June 29, 2007, with the sales of the first personal, digital hand-held device that connected to the internet – the iPhone. With the iPhone, for the first time, consumers could view and post to their social media accounts anywhere, anytime. Social media was no longer a location-restricted, home-bound activity on a computer.

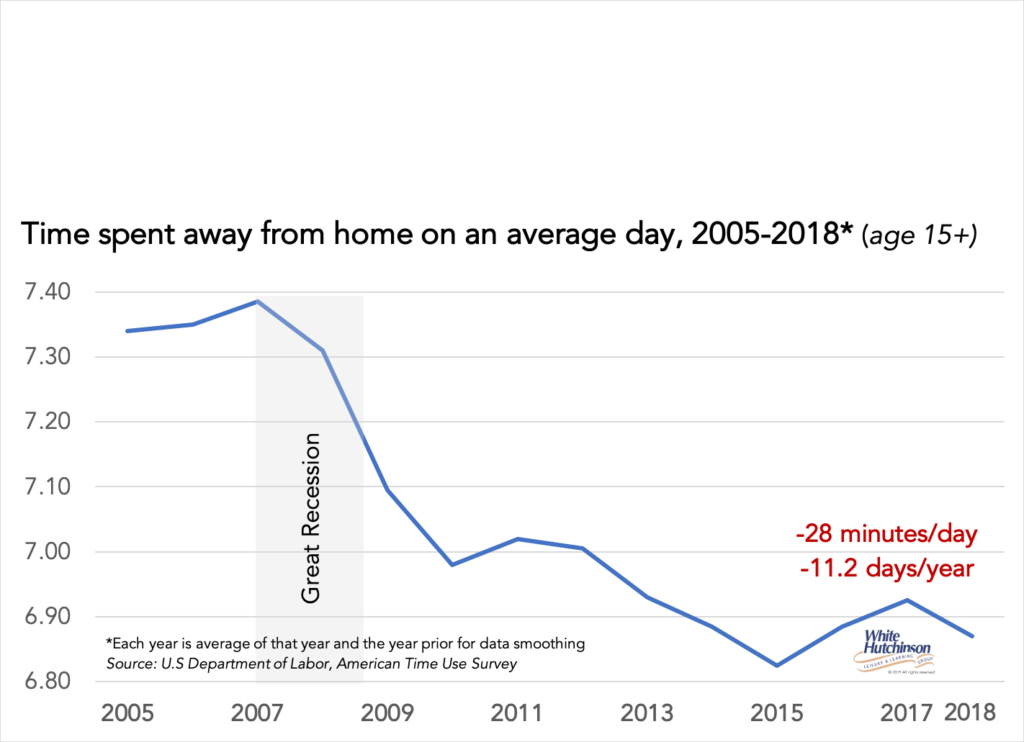

The third pivotal event was the Great Recession that began December 2007 and continued until June 2009. The Great Recession and the resulting financial distress and anxiety consumers experienced brought on an abrupt sea change of an increase in time spent at home and a decrease in time spent away from home, which hasn’t recovered since. Between 2007 and 2010, consumers age 15+ decreased their time away from home by 24 minutes a day and it continued to decline 31 minutes less time per day away from home in 2018 than in 2007. That’s the equivalent to more than twelve less waking days a year away from home.

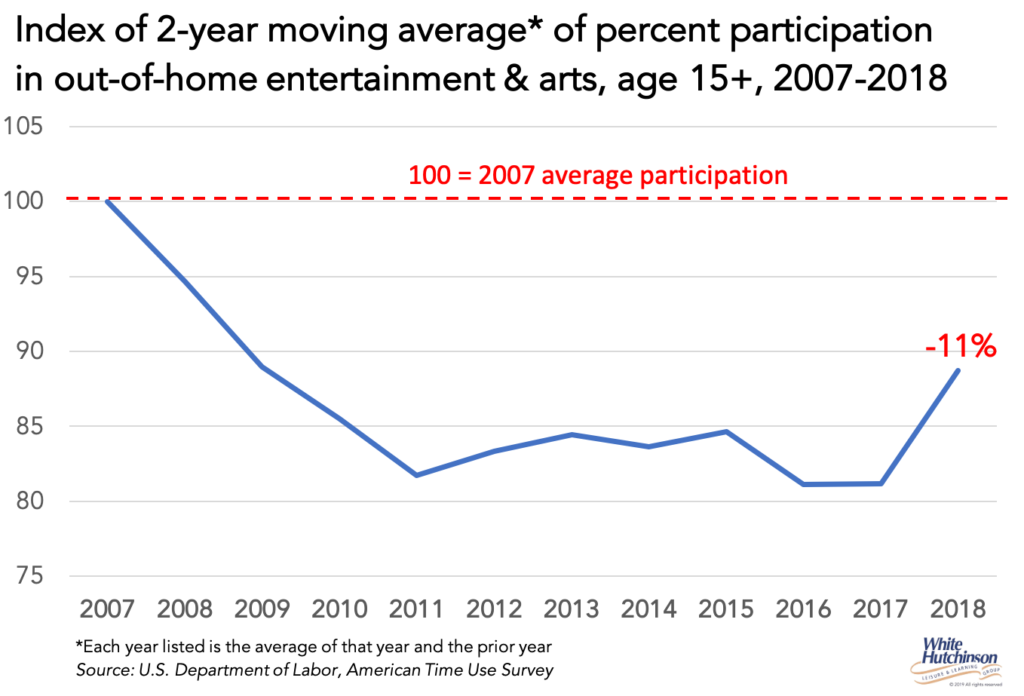

Impact from e-commerce, telecommuting, mobile banking and other activities that can now be digitally accomplished at home has contributed to the increase in time spent at home and decreased time away. At the same time, people also increased the time they spend on at-home digital entertainment, and decreasing their attendance and time spent at out-of-home entertainment and art venues (OOH E&A). Since 2007, the average percentage of age 15+ attending OOH E&A on an average day has declined by 11 percent.

Impact from e-commerce, telecommuting, mobile banking and other activities that can now be digitally accomplished at home has contributed to the increase in time spent at home and decreased time away. At the same time, people also increased the time they spend on at-home digital entertainment, and decreasing their attendance and time spent at out-of-home entertainment and art venues (OOH E&A). Since 2007, the average percentage of age 15+ attending OOH E&A on an average day has declined by 11 percent.

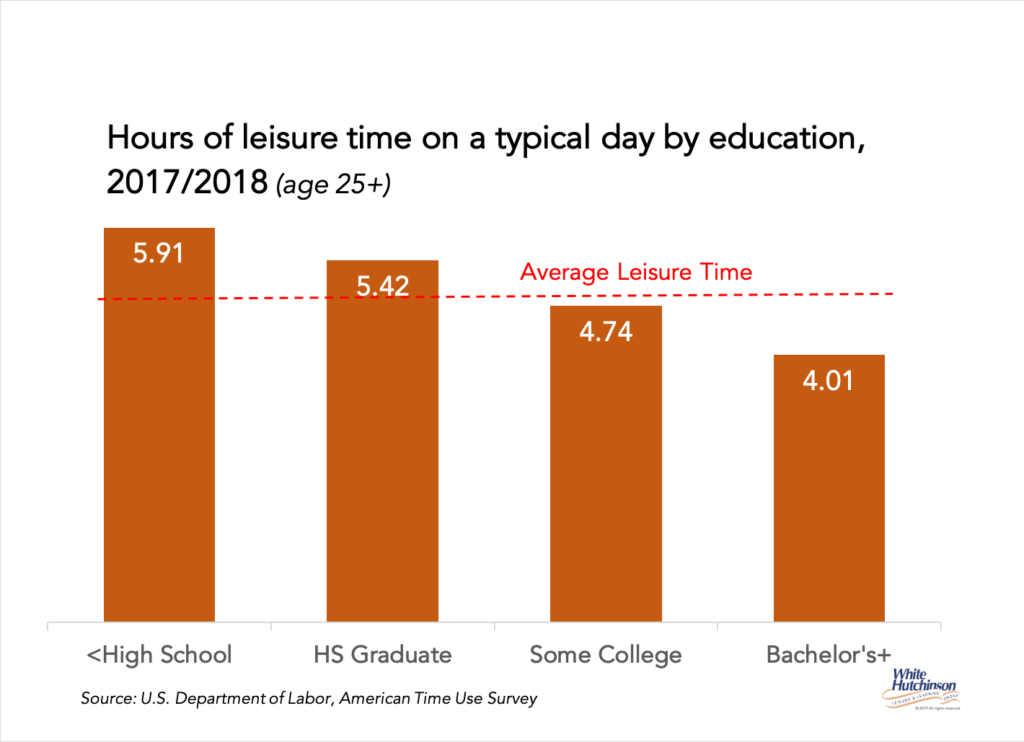

Time spent at OOH E&A still hasn’t recovered to pre-recession levels. Annual attendance for age 15+ is down by one-half less visits per year than in 2007. Time spent has not recovered for the middle and lower socio-economic classes, while it has for the higher socio-economic. Bachelor’s and higher-degreed adults age 25+ now account for half of all time spent at E&A venues, yet make up only one-quarter of 25-and-older adults.

The Great Recession also brought on more frugal entertainment spending. Consumers shifted to less-expensive, at-home, digital entertainment options – watching their big screen TVs and playing video games – rather than visiting OOH E&A venues. The cost of streaming movies or a TV series, or playing a video game, is only a few cents per hour whereas going to an out-of-home location can cost many dollars per hour. And by staying home, you didn’t have to spend any of your limited leisure time traveling to and from some venue.

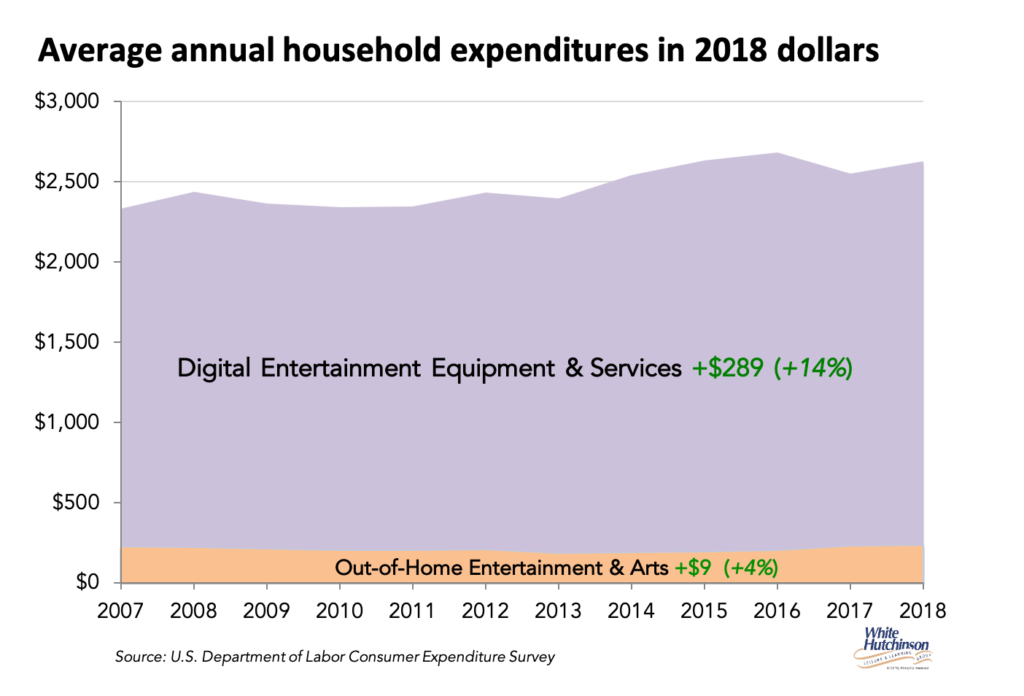

Since 2007, digital entertainment spending for equipment and services has continued to grow at multiples of the growth for OOH E&A. At-home and personal screen entertainment spending is now more than 10 times the spending on OOH E&A fees and admissions.

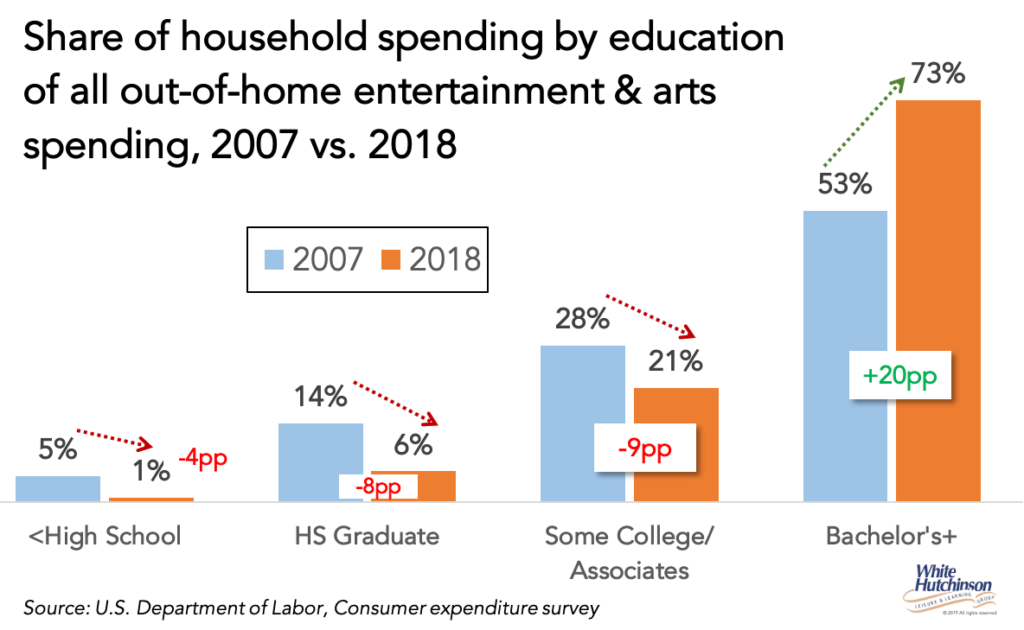

It’s only in the past few years that average household spending for OOH E&A has recovered to its pre-recession level, but even then, no different than for time, it hasn’t recovered for the middle- and lower socio-economic classes. Average household spending is up solely due to an increase in spending by higher-socioeconomic households. Bachelor’s and higher degree households have grown from a little over half of all OOH E&A spending in 2007 (53 percent) to almost three-quarters in 2018 (73 percent). Spending continues to be down for the middle class and lower-education households.

It’s only in the past few years that average household spending for OOH E&A has recovered to its pre-recession level, but even then, no different than for time, it hasn’t recovered for the middle- and lower socio-economic classes. Average household spending is up solely due to an increase in spending by higher-socioeconomic households. Bachelor’s and higher degree households have grown from a little over half of all OOH E&A spending in 2007 (53 percent) to almost three-quarters in 2018 (73 percent). Spending continues to be down for the middle class and lower-education households.

What has transpired over the 12 years is a gentrification of both OOH E&A time and spending.

Powerful Changes

As significant as the shift from out-of-home to at-home entertainment participation, time and spending entertainment has been since 2007, the three pivotal events have also brought on a seismic change in the culture of out-of-home entertainment that has had an even more momentous impact.

The fourth level of Maslow’s Hierarchy of Needs is “esteem, recognition and respect.” Prior to the introduction of the smartphone and its use for social media, conspicuous consumption of things was the predominant way people gained status, whether it was some logo on their clothing, the car they parked in their driveway, the watch they wore or the purse they carried. Gaining status for owning status-worthy things wasn’t immediate as it took time for a person’s social-signaling group to be exposed to and see those items. The smartphone and its ability to instantly post and broadcast to all your social media followers, photos of envious experiences you are having while you are having them accelerated the transition to the experience economy, as well as a shift from the conspicuous consumption of stuff to conspicuous leisure consumption.

This brought on a shift of peoples’ identity from “I am what I own” to “I am what I do.” Now, two-thirds of people would rather be known for their experiences than their possessions. Signaling your identity and gaining social capital has shifted to the experiences we have and post on social media. Today, the majority of people are collecting experiences that are documented by their social media postings as their Experiential CVs, predominately on Instagram and Facebook. In fact, for many people, especially younger adults, if some entertainment experience isn’t “Instagrammable,” it probably isn’t worth doing.

The more status-worthy experiences you can post, the greater your social capital. Once a particular experience is posted, it no longer has value to repeat. So, people are constantly seeking new and unique experiences their social media followers haven’t experienced, will be envious of and will want to do “to keep up with the Joneses.” For one- and limited-time events, those postings especially trigger FOMO (fear of missing out).

In addition to the social capital appeal of unique experiences, evolution wired our brains to crave novelty, as new experiences cause the release of dopamine, the feel-good neurotransmitter that gives us pleasure.

People today are looking for the perfect ‘Gram.’ Research shows that they are willing to visit and spend more money than they would otherwise on some experience that has a high conspicuous leisure Instagrammable value, especially ones that will trigger FOMO with their followers.

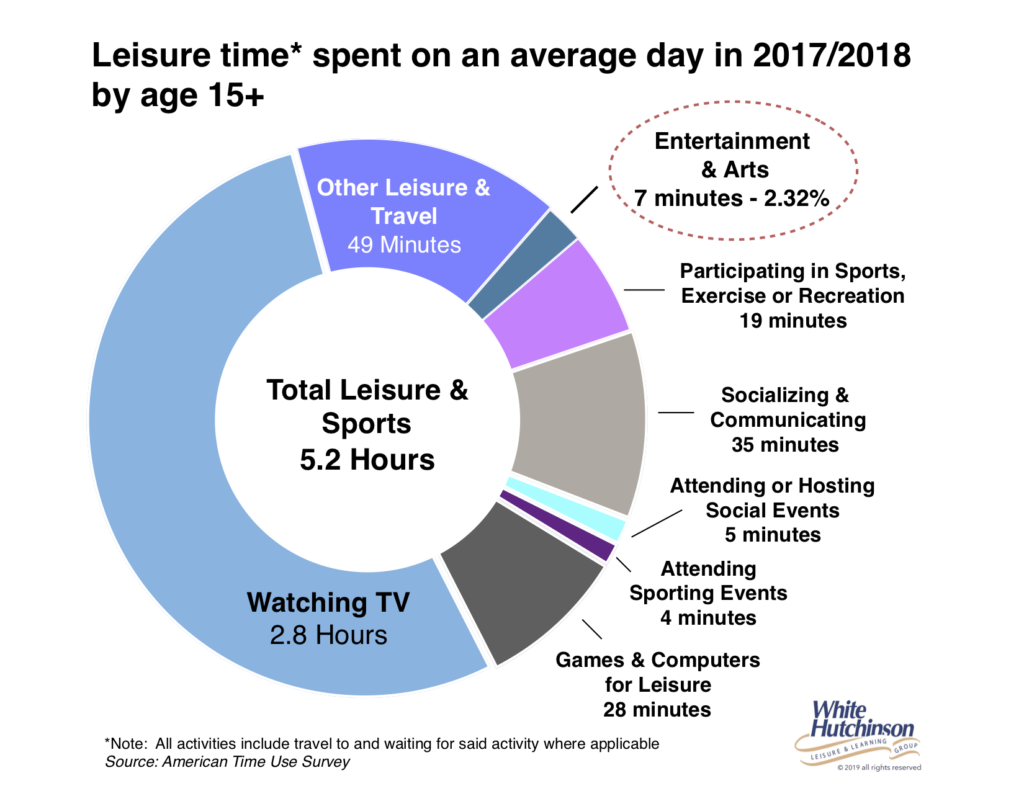

Many people today are experiencing time pressure. The truth is that the amount of leisure time people have, on average 5.2 hours a day, hasn’t really changed for decades other than minor fluctuations of a few minutes from year to year. One theory of why people feel time pressured is that there are so many options of what they can do today, but not enough time to do them all. People who are the most time pressured are the higher socioeconomic who have the least amount of leisure time each day.

Many people today are experiencing time pressure. The truth is that the amount of leisure time people have, on average 5.2 hours a day, hasn’t really changed for decades other than minor fluctuations of a few minutes from year to year. One theory of why people feel time pressured is that there are so many options of what they can do today, but not enough time to do them all. People who are the most time pressured are the higher socioeconomic who have the least amount of leisure time each day.

People with higher status engage in what is called “voracious leisure consumption,” making the most productive use of their leisure time, using their leisure time “to its fullest,” pursuing and experiencing as many of the vast variety of OOH leisure and entertainment options the world now offers at the highest frequency possible. Professionals, adults living alone and post-college, pre-kids younger couples tend to be most voracious in their leisure participation.

Of all the 5.2 hours of leisure time people age 15+ have each day, just a small portion –– only slightly more than 2 percent or an average of 7 minutes a day –– is devoted to OOH E&A. That compares with 28 minutes a day on average being spent using digital devices, playing video games or for leisure (not including the 2.8 hours a day of TV time). And OOH E&A time is inelastic. More options do not increase the share of total leisure time people will spend attending OOH E&A. As previously shown, that time and their number of visits to OOH E&A has actually decreased since 2007. So, for OOH E&A, it’s a zero sum game, and a smaller one than in the past.

Over the past few years, shopping center and mall landlords, trying to fill vacant retail stores and generate foot traffic, and entrepreneurs thinking location-based entertainment is a fun and easy road to riches (it’s actually a very complex and challenging business to run successfully) have brought on a massive explosion in the variety and the number of LBE options in almost all markets. These include, just to name a few, trampoline parks, FECs, indoor sky diving, adventure parks, escape rooms, zip line experiences, bar arcades, eSport lounges, axe throwing, social eatertainment centers with participatory games and destination-worthy food and drink such as Punch Bowl Social and Top Golf, eatertainment venues where you can bring your dog, VR, corn mazes/pumpkin patches, golf-swing suites, cocktails and mini-golf. Additionally, there has been a growing explosion in the number and variety of non-attraction OOH entertainment including festivals of all types, live events, foodie-worthy restaurants, food truck meet-ups, breweries, distilleries and wineries, all that satisfy conspicuous and voracious leisure consumption and compete for the zero-sum game of OOH entertainment time and spending.

Over the past few years, shopping center and mall landlords, trying to fill vacant retail stores and generate foot traffic, and entrepreneurs thinking location-based entertainment is a fun and easy road to riches (it’s actually a very complex and challenging business to run successfully) have brought on a massive explosion in the variety and the number of LBE options in almost all markets. These include, just to name a few, trampoline parks, FECs, indoor sky diving, adventure parks, escape rooms, zip line experiences, bar arcades, eSport lounges, axe throwing, social eatertainment centers with participatory games and destination-worthy food and drink such as Punch Bowl Social and Top Golf, eatertainment venues where you can bring your dog, VR, corn mazes/pumpkin patches, golf-swing suites, cocktails and mini-golf. Additionally, there has been a growing explosion in the number and variety of non-attraction OOH entertainment including festivals of all types, live events, foodie-worthy restaurants, food truck meet-ups, breweries, distilleries and wineries, all that satisfy conspicuous and voracious leisure consumption and compete for the zero-sum game of OOH entertainment time and spending.

Today, many Millennials, as well as other age adults, prefer to go to a restaurant over the movies, concert, cultural or live events. Restaurants, breweries, distilleries and wineries and other food and drink experiences have become the “new entertainment.” More than half of people (51 percent) now consider dining in a restaurant as entertainment.

As a result of the change in consumers’ preferences for new, unique, socially-shareable, out-of-home leisure experiences, a whole new category of OOH E&A experiences have emerged –– immersive pop-up museums and art exhibits specially designed to offer highly interactive and Instagrammable experiences. Examples include Meow Wolf, The Ice Cream Museum, Snark Park, Natura Obscura, Candytopia and themed, pop-up cocktail bars.

As a result of conspicuous and voracious leisure driving Instagram-worthy variety seeking, the culture of OOH E&A has shifted from the repeat appeal attractions had not that many years ago to unique and one- and limited-time events such as live events, festivals and concerts. These are the experiences that are now winning a greater share of people’s OOH time and wallets. With so many unique experiences to do instead, attraction-based venues have lost much of their repeat appeal –– “been there, done that.”

PGAV in recent research found that every type of attraction, whether they are museums, zoos, theme parks, FECs, water parks, aquariums or science centers, to name just a few types they researched, have declined in repeat appeal. Rather, they found a growing appeal of what they call “the attraction of the non-attraction,” the growth in attendance to live, one- and limited-time events.

Between 2007 and 2018, total spending (inflation-adjusted) for live entertainment has increased by 25 percent, whereas for non-live entertainment venues and parks, it only grew by 13 percent.

There is one additional phenomenon that is contributing to the decline in repeat appeal. People enjoy OOH E&A experiences less and less the more times they repeat the same one. The second time you enjoy an E&A experience, it isn’t as good as the first, and the third time isn’t as good as the second. The more people do a particular experience, the more likely they are to get bored with it (again, “been there, done that”) and the more likely they are to move on to some new entertainment experience to enjoy.

As a result, OOH E&A experiences “self-commoditize” through people’s repeat visits. Combined with social media postings of all the new, unique entertainment options, and the FOMO it creates, accelerates the commoditization of OOH E&A experiences. Today, in many situations, OOH E&A experiences, especially ones based on attractions, become commoditized after just one visit. They have no repeat appeal since there are so many new things people are trying to do in their limited leisure time to add to their Experiential CVs.

It’s Got Our Attention

Over the past couple of years, our company has been hired by a number of existing attraction-based entertainment venues experiencing declining attendance to advise them on how they could grow their attendance and revenues. We analyzed the attendance and revenues of 13 different centers open at least two years. For all but one, including those for a well-respected chain, we found a decline in overall attendance, predominately attributable to a decline in repeat attendance.

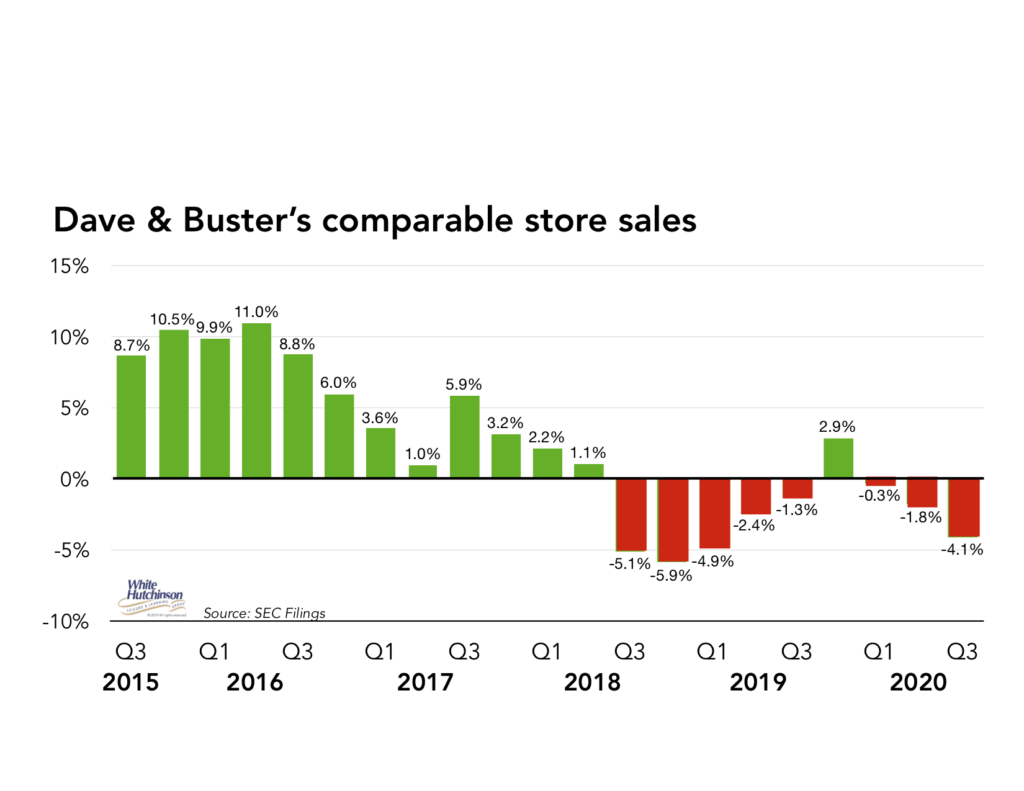

Even evergreen chains such as Dave & Buster’s are experiencing the disruptive shifting culture of OOH E&A to variety seeking rather than repeat visits. Adjusted for inflation, D&B’s same store sales were down 3.4 percent in 2018 and are projected to be down around 4 percent in 2019. D&B reported that in the third quarter of their 2019 fiscal year, 45 percent of their stores open more than one year have seen declining sales due to either new competition or cannibalization.

Even evergreen chains such as Dave & Buster’s are experiencing the disruptive shifting culture of OOH E&A to variety seeking rather than repeat visits. Adjusted for inflation, D&B’s same store sales were down 3.4 percent in 2018 and are projected to be down around 4 percent in 2019. D&B reported that in the third quarter of their 2019 fiscal year, 45 percent of their stores open more than one year have seen declining sales due to either new competition or cannibalization.

The OOH entertainment and arts consumer, their preferences, expectations, values and behaviors have dramatically changed from a dozen years ago. As a result, there has been a transformative and disruptive sea change to the culture of out-of-home entertainment. Market share has shifted away from traditional brick-and-mortar business models, focused on fixed attractions, to an expanding number and variety of new-type venues, especially to one- and limited-time, live, new and unique OOH experiences, including many food and beverage experiences.

Heavily influenced by the values of the experience economy, conspicuous and voracious leisure and social media, repeat appeal is losing out to “been there, done that” and the desire to move on to the greatly expanded landscape of all the new and socially sharable OOH experiences options that are now capturing consumers’ attention, time and money. As the result, the traditional business model for brick-and-mortar E&A venues with a predominate focus on attractions as the draw is no longer a sustainable business model. Yes, people might come the first time, but attractions have lost the long-term repeat appeal they once had. It’s no longer just about the attractions, although the attractions can still be a part of the overall experience. The appeal of the overall experience, whether it is compelling enough to visit, is now judged on so much more than the attractions.

Today, the winning formula for OOH E&A has become a lot more complex. Today, it’s all about a total share-worthy experience that includes quality discovery and adventure food and drink, a great design and atmosphere, great hospitality, and continually changing reasons to return.

© 2020 White Hutchinson Leisure & Learning Group

The White Hutchinson Leisure & Learning Group is a multi-disciplinary firm specializing in feasibility, concept and brand development, design and consulting for entertainment facilities. Over the past 26 years, the company has worked for over 500 clients in 32 countries, and won 16 first-place design awards. It publishes an occasional Leisure eNewsletter and Tweets (@whitehutchinson); Randy blogs. He is also a founder, co-regent and presenter at Foundations Entertainment University, now in its 13th year. Randy can be reached at 816/931-1040, ext. 100, or via the company’s website at www.white hutchinson.com. © 2015 White Hutchinson Leisure & Learning Group